Important information for SMSF Trustees: Understanding NALI and NALE

Non-Arm’s Length Income (NALI) and Non-Arm’s Length Expenses (NALE)

NALI and NALE are critical concepts for Self-Managed Superannuation Funds (SMSFs). They exist to ensure all transactions are conducted on commercial, arm’s-length terms, as required by the Superannuation Industry (Supervision) Act 1993 (SIS Act). Breaching these rules can lead to severe tax penalties and compliance risks.

What is NALI?

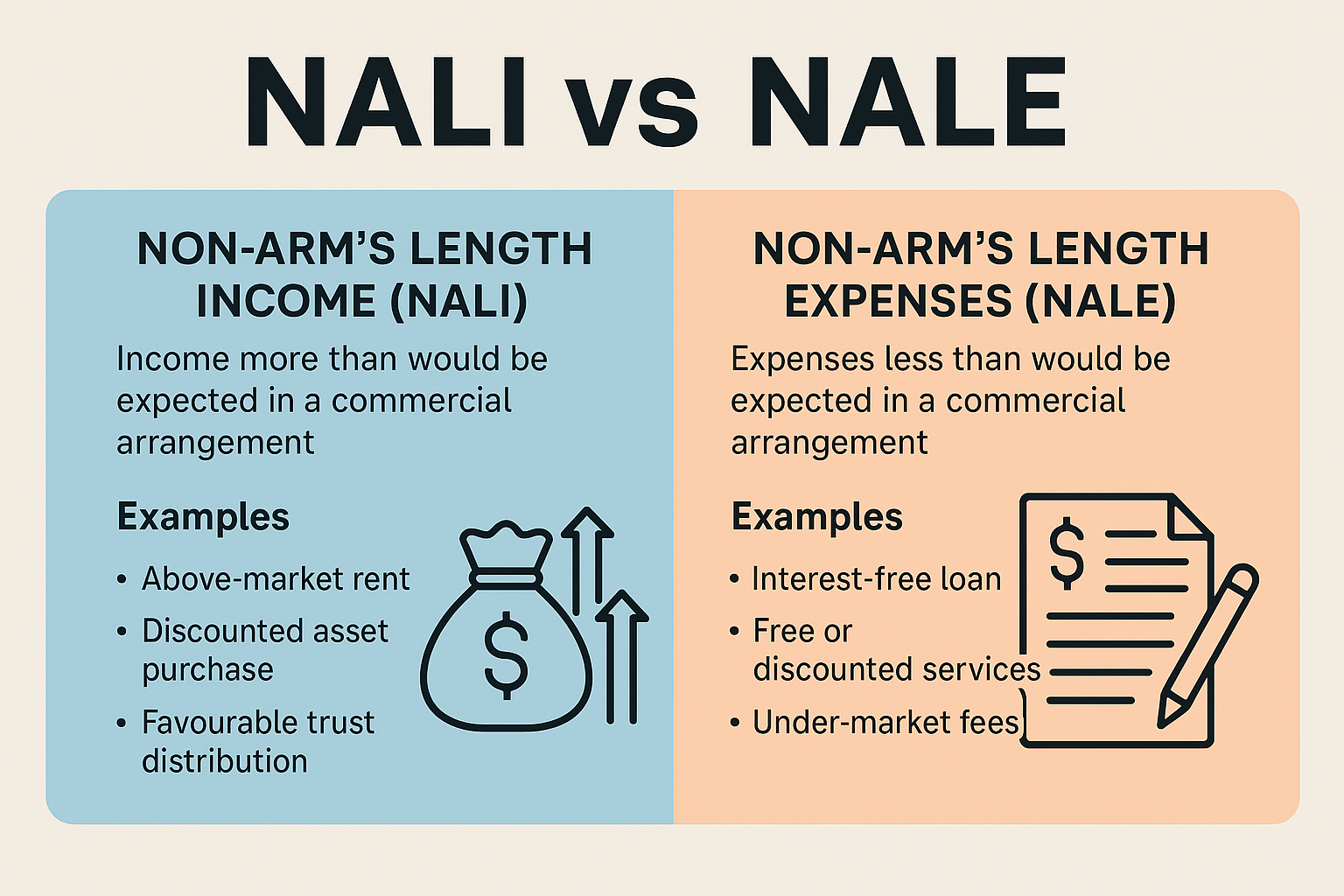

NALI occurs when an SMSF earns more income than it would if the parties are dealing at arm’s length. Common examples include:

Above-market rent: Leasing a property to a related party at more than the market rate.

Discounted asset purchase: Buying an asset from a related party at a significant discount and earning inflated returns.

Favourable trust distributions: Receiving disproportionate benefits from a trust compared to other beneficiaries.

What is NALE?

NALE refers to expenses that the SMSF pays less for than would be expected or does not pay for them at all, giving the SMSF an unfair advantage. Examples include:

Interest-free loans: A related party lends money to the SMSF without charging interest (e.g. this can happen when a trustee or member pays an expense on behalf of the SMSF and does not get reimbursed, or, is reimbursed after more than seven days).

Free or discounted services: Trustees or related parties provide services to the SMSF for free or lower than what would be expected if an unrelated party provided the services (e.g. a builder making repairs to a property that their SMSF owns and not charging for it).

Under-market fees: Paying significantly less for investment management or audit services.

Why It Matters

Breaching NALI/NALE rules triggers harsh consequences:

Tax penalty: Income deemed NALI is taxed at 45%, not the usual 15% (or 0% in pension phase).

Specific vs General NALE:

Specific NALE taints income from the affected asset (including future capital gains).

General NALE can impact all fund income. Recent legislative changes have placed a cap on the amount of the income that is taxed at higher rates; however, it remains a significant penalty.

Compliance risks: Breaches violate the SIS Act, risking trustee fines and, in severe cases, the fund being declared non-complying, which could materially reduce the fund’s assets.

How to Stay Compliant

Always transact at market value (arm’s length): Use independent valuations and written agreements.

Avoid “mates’ rates”: Free or discounted services can trigger NALE unless they are incidental trustee duties.

Document everything: Keep records to demonstrate all dealings with the Fund are at arm’s-length.

Stay informed: ATO guidance and legislative changes (such as 2024 amendments) have refined these rules— ensure you’re up to date.

Key Takeaway

Short-term savings or benefits from non-arm’s length deals can lead to devastating tax bills and compliance issues, ask yourself: ‘Would this arrangement stand up to ATO scrutiny as a commercial deal’? If not, rethink or seek professional advice.

Need help navigating SMSF compliance? Contact our team at Acumen Accounting & Business Services for expert guidance on keeping your fund safe and compliant.